Chindia Alert: You’ll be Living in their World Very Soon

aims to alert you to the threats and opportunities that China and India present. China and India require serious attention; case of ‘hidden dragon and crouching tiger’.

Without this attention, governments, businesses and, indeed, individuals may find themselves at a great disadvantage sooner rather than later.

The POSTs (front webpages) are mainly 'cuttings' from reliable sources, updated continuously.

The PAGEs (see Tabs, above) attempt to make the information more meaningful by putting some structure to the information we have researched and assembled since 2006.

In Wuhan, the epicentre of China’s outbreak, all traffic lights in urban areas were turned red at 10:00, ceasing traffic for three minutes.

China’s government said the event was a chance to pay respects to “martyrs”, a reference to the 14 medical workers who died battling the virus.

Image copyright GETTY IMAGESImage caption China came to a standstill during the three-minute silence at 10:00 local time

They include Li Wenliang, a doctor in Wuhan who died of Covid-19 after being reprimanded by the authorities for attempting to warn others about the disease.

“I feel a lot of sorrow about our colleagues and patients who died,” a Chinese nurse who treated coronavirus patients told AFP news agency. “I hope they can rest well in heaven.”

Wearing white flowers pinned to their chest, Chinese President Xi Jinping and other government officials paid silent tribute in Beijing.

Saturday’s commemorations coincide with the annual Qingming festival, when millions of Chinese families pay respects to their ancestors.

China first informed the World Health Organization (WHO) about cases of pneumonia with unknown causes on 31 December last year.

By 18 January, the confirmed number of cases had risen to around 60 – but experts estimated the real figure was closer to 1,700.

Image copyright GETTY IMAGESImage caption China’s government said the commemoration was held to pay respects to “martyrs”

Just two days later, as millions of people prepared to travel for the lunar new year, the number of cases more than tripled to more than 200 and the virus was detected in Beijing, Shanghai and Shenzhen.

From that point, the virus began to spread rapidly in Asia and then Europe, eventually reaching every corner of the globe.

Media caption The BBC met people in Beijing heading out after the lockdown

In the past few weeks, China has started to ease travel and social-distancing restrictions, believing it has brought the health emergency under control.

Last weekend, Wuhan partially re-opened after more than two months of isolation.

On Saturday, China reported 19 new confirmed cases of coronavirus, down from 31 a day earlier. China’s health commission said 18 of those cases involved travellers arriving from abroad.

As it battles to control cases coming from abroad, China temporarily banned all foreign visitors, even if they have visas or residence permits.

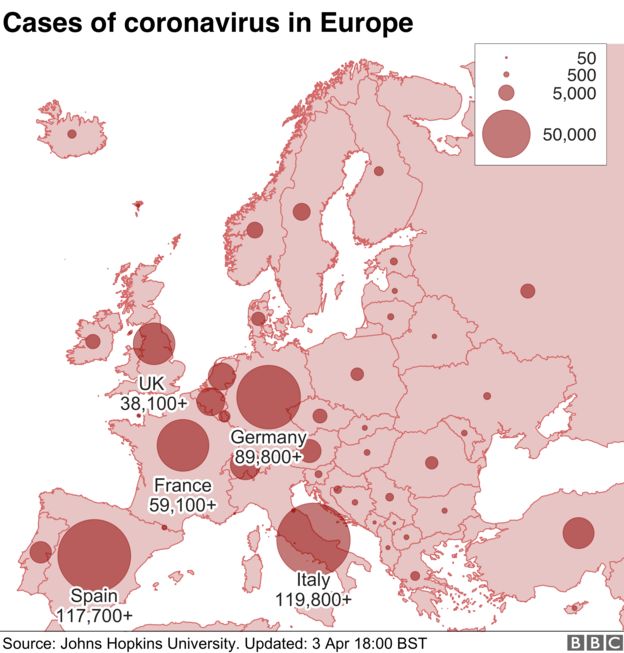

What is the latest worldwide?

As the coronavirus crisis in China abates, the rest of the world remains firmly in the grip of the disease.

The deaths increased by 1,480 in 24 hours, the highest daily death toll since the pandemic began, AFP news agency reported, citing Johns Hopkins University’s case tracker.

The head of the International Monetary Fund (IMF) said the pandemic has bought the global economy to a standstill, causing a recession “way worse than the global financial crisis” of 2008

The United Nations appealed to governments around the world not to use the pandemic as an excuse to stifle dissent

BEIJING, March 27 (Xinhua) — As the novel coronavirus disease (COVID-19) makes social distancing and working from home the new normal, leaders of the Group of 20, home to almost two-thirds of the world’s population and about 86 percent of the gross world product, convened Thursday for a virtual summit that sent a clear message: We are in the same boat.

The G20 Extraordinary Virtual Leaders’ Summit on COVID-19 was the first of its kind in the history of G20, and also the first major multilateral event attended by President Xi Jinping since the outbreak of the COVID-19.

Speaking to his colleagues via video link from Beijing, Xi put forward four proposals to cope with a situation that is “disturbing and unsettling,” calling for an all-out global war against the COVID-19 outbreak and enhancing international macro-economic policy coordination to prevent a recession.

“At such a moment, it is imperative for the international community to strengthen confidence, act with unity and work together in a collective response,” Xi said. “We must comprehensively step up international cooperation and foster greater synergy so that humanity as one could win the battle against such a major infectious disease.”

In a demonstration of the need for greater global coordination and solidarity, the G20 members were joined by leaders from invited countries including hard-hit Spain as well as multiple international organizations including the United Nations (UN), the World Health Organization (WHO), the World Trade Organization (WTO), and the International Monetary Fund (IMF).

While previous G20 summits often discussed high-stake topics like economic recession and boosting development policy, Thursday’s emergency meeting came at a time when the world is grappling with a dicey pandemic and concerns are mounting over the “black swan” event that could derail the global economy.

As China’s epidemic prevention and control are continuously improving, and the trend of an accelerated restoration of normal production and life is being consolidated and expanded, his remarks at the G20 summit are timely and of critical importance for countries now fighting at the front lines of a battle to stem the pandemic and forestalling a recession.

UNITED WE STAND

The number of COVID-19 cases worldwide topped 462,684, with 20,834 deaths as of 10 a.m. Central European Time, Thursday, according to the data kept by the WHO. The economic toll is also climbing as more businesses and trade come to a grinding halt amid massive lockdowns.

“The COVID-19 pandemic is endangering countries rich and poor, large and small, strong and weak alike,” said Wei Jianguo, vice chairman of the China Center for International Economic Exchanges and former vice minister of Commerce. “We are now at a critical juncture of fighting the pandemic and stabilizing the global economy, and the international community expects the G20 to play a leading role.”

The significance and urgency of Thursday’s meeting hark back to scenarios in the depth of the global financial crisis in 2008 when meetings of G20 finance ministers and central bank governors were raised to the level of heads of state and government for better crisis coordination. What’s different is that grave challenges facing the world today have led to warnings of a downturn even worse than in 2008.

“This pandemic will inevitably have an enormous impact on the economy,” WTO Director-General Roberto Azevedo said in a video clip posted on the website of the organization. “Recent projections predict an economic downturn and job losses that are worse than the global financial crisis a dozen years ago.”

To prevent the world economy from falling into recession, Xi said countries need to leverage and coordinate their macro policies to counteract the negative impact as the outbreak has disrupted production and demand across the globe.

“We need to implement strong and effective fiscal and monetary policies to keep our exchange rates basically stable. We need to better coordinate financial regulation to keep global financial markets stable. We need to jointly keep the global industrial and supply chains stable,” he told the summit in a speech titled “Working Together to Defeat the COVID-19 Outbreak.”

Xi’s remarks on fighting as one echoed. IMF Managing Director Kristalina Georgieva said: “We project a contraction of global output in 2020, and recovery in 2021. How deep the contraction and how fast the recovery depends on the speed of containment of the pandemic and on how strong and coordinated our monetary and fiscal policy actions are.”

“We will get through this crisis together. Together we will lay the ground for a faster and stronger recovery,” she said in a statement released after the conference call.

The important lesson in international solidarity is often forgotten when things are going fine, William Jones, Washington bureau chief of the U.S. publication Executive Intelligence Review, told Xinhua in a recent interview.

“The experience with the COVID-19 will hopefully lead to more collaborative efforts between countries and strengthen the notion of a community with a shared destiny,” he said.

As China is a key driver of global economic growth, its economic performance bears great significance on the outlook of global recovery. In a strong morale and practical boost, Xi reaffirmed China would actively contribute to the global war against COVID-19 and a stable world economy.

“Guided by the vision of building a community with a shared future for mankind, China will be more than ready to share its good practices, conduct joint research and development of drugs and vaccines, and provide assistance where it can to countries hit by the growing outbreak,” Xi said.

Xi said China will contribute to a stable world economy by continuing to advance reform and opening-up, widen market access, improve the business environment and expand imports and outbound investment, and called on all G20 members to take collective actions — cutting tariffs, removing barriers, and facilitating the unfettered flow of trade.

The country is beefing up wider opening-up to foreign investment. Revision of the negative list on foreign investment is underway as part of the plan to improve business environment and expand the catalog of industries where foreign investment is encouraged.

New editions of the list will probably be released in May, expanding market access of the tertiary sector, such as health care, aged service, finance, transportation, logistics, tourism, education and training and value-added services of telecommunications, said Zhang Fei with the Chinese Academy of International Trade and Economic Cooperation.

Noting that a global solution is needed to address the global challenge brought about by the pandemic, Azevedo said cross-border trade and investment flows have a role to play in efforts to combat the COVID-19 pandemic and will be vital for fostering a stronger recovery once the medical emergency subsides.

“No country is self-sufficient, no matter how powerful or advanced it may be. Trade is what allows for the efficient production and supply of basic goods and services, medical supplies and equipment, food and energy that we all need,” he said.

Chinese Premier Li Keqiang and leaders of six major international economic and financial institutions meet the media after their fourth roundtable meeting in Beijing, capital of China, Nov. 21, 2019. The six leaders are World Bank Group President David Malpass, International Monetary Fund Managing Director Kristalina Georgieva, World Trade Organization Deputy Director-General Alan Wolff, International Labor Organization Director-General Guy Ryder, Organization for Economic Cooperation and Development Secretary-General Angel Gurria and Financial Stability Board Chairman Randal Quarles. (Xinhua/Yue Yuewei)

BEIJING, Nov. 21 (Xinhua) — Chinese Premier Li Keqiang held a roundtable meeting with leaders of six major international economic and financial institutions in Beijing on Thursday.

The six leaders are World Bank Group President David Malpass, International Monetary Fund Managing Director Kristalina Georgieva, World Trade Organization Deputy Director-General Alan Wolff, International Labor Organization Director-General Guy Ryder, Organization for Economic Cooperation and Development Secretary-General Angel Gurria and Financial Stability Board Chairman Randal Quarles.

Li expressed hope to build consensus, boost confidence and deepen cooperation through the meeting, so as to promote the sustained, healthy and stable development of world economy.

It is the fourth roundtable meeting for Li and leaders of the six institutions. This year’s meeting features the theme of “promoting openness, stability and high-quality development of the world economy.”

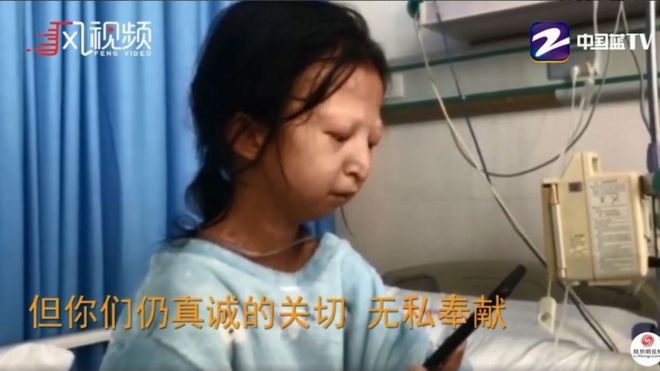

Image copyright FENG VIDEOImage caption Wu Huayan ate only rice and chillies in order to save money to help her ill brother

Well-wishers have donated almost a million yuan to a Chinese student who was hospitalised after living on 2 yuan ($0.30, £0.20) a day for five years.

The case of Wu Huayan shocked Chinese people after it hit the headlines earlier this week.

The 24-year old woman became seriously malnourished while struggling to study and support her sick brother.

Ms Wu’s story also sparked anger at authorities for failing to recognise her plight and help her much earlier.

After the story was reported, donations began pouring in for the college student in the city of Guiyang – reportedly totalling some 800,000 yuan ($114,000, £88,000).

What is Wu Huayan’s story?

Earlier, this month, the young woman went into hospital after having difficulty breathing, according to Chinese media.

She was only 135cm (4ft 5ins) tall, weighing barely more than 20kg (43 pounds; three stones).

The doctors found she was suffering from heart and kidney problems due to five years spent eating minimal amounts of food. She said she needed to save money to support her sick brother.

Wu Huayan lost her mother when she was four and her father died when she was in school.

She and her brother were then supported by their grandmother, and later by an uncle and aunt who could only support them with 300 yuan ($42, £32) each month.

Most of that money went on the medical bills of her younger brother, who had mental health problems.

This meant Ms Wu spent only 2 yuan a day on herself, surviving largely off chillies and rice.

The siblings are from Guizhou, one of the poorest provinces in China.

Media caption China’s uphill struggle fighting extreme poverty

What has the reaction been?

The case sparked an outpouring of concern – and anger at authorities.

Many people on social media said they wanted to help with donations, and many voiced concern about her college not helping her.

One user called her situation “worse than that of refugees in Afghanistan”, while another pointed to the extravagant cost of China’s 70th anniversary celebrations, saying the money could have been better spent.

Others expressed their admiration at her efforts to help her brother, while also persevering with her studies in college.

Aside from the donations on crowd funding platforms, her teachers and classmates donated 40,000 yuan ($5,700; £4,400), while local villagers collected 30,000 yuan to help her.

Officials released a statement saying Ms Wu had been receiving the minimum government subsidy – thought to be between 300 and 700 yuan a month – and was now getting an emergency relief fund of 20,000 yuan.

“We will keep following the case of this strong-minded and kind girl,” the Tongren City Civil Affairs Bureau said.

“We will actively co-operate with other relevant departments to solve the problem according to the minimum living standard and temporary assistance responsibility that the civil affairs department bears.”

Dubbed “Little Wang”, his story also went viral, leading to international donations from people impressed by his resilience, and shocked at his poverty.

Image copyright PEOPLE’S DAILY

While China’s economy has skyrocketed over the past decades, poverty has not disappeared, and inequality has grown.

One major reason cited is the huge divide between rural and urban areas.

As a point of comparison, in rural region of Guizhou where Ms Wu lives, that figure is around 16,703 yuan.

China has moved from being “moderately unequal in 1990 to being one of the world’s most unequal countries,” according to a 2018 report by the International Monetary Fund.

According to the National Bureau of Statistics in 2017, 30.46 million rural people were still living below the national poverty line of $1.90 a day.

China has previously pledged to “eliminate” poverty by 2020.

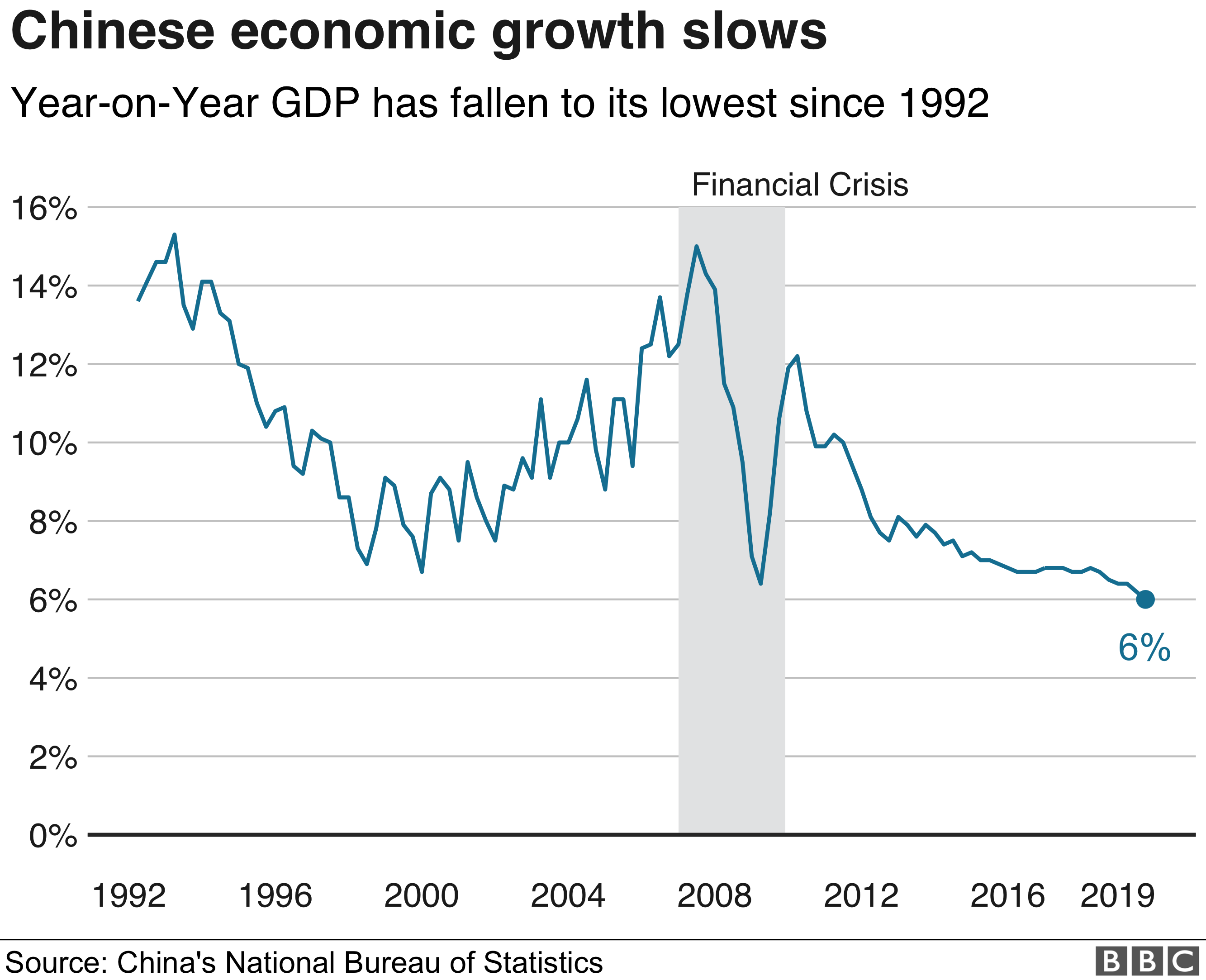

China’s economy grew at a slower pace than expected in the third quarter as it struggled with a US-led trade war and softer domestic demand.

In the three months to September, the economy expanded 6% from a year earlier, official figures showed.

The result fell just short of expectations for 6.1% growth for the period.

The slowdown comes despite government efforts to support the economy, including measures such as tax cuts.

The latest figures mark a further loss of momentum in the world’s second largest economy, which had already seen growth languishing at its slowest pace in around three decades.

The rate remained within the government’s target range for annual growth of between 6% and 6.5%.

The strength of the Chinese economy is closely watched as slowing growth can have far-reaching consequences for the global economy.

The country has become a key engine of growth in recent decades. Its healthy demand for a range of products, from commodities to machinery, has supported growth around the world.

Some analysts worry that a sharp slowdown in China could hurt an already sluggish world economy and increase the risk of a recession.

Julian Evans-Pritchard, senior China economist at Capital Economics, said pressure on the Chinese economy “should intensify in the coming months”.

He said more intervention by policymakers to support the economy was likely “but it will take time for this to put a floor beneath economic growth”.

What challenges does China face?

China has been fighting a trade war with the US for the past year, which has created uncertainty for businesses and consumers.

At the same time, it faces domestic challenges including a swine fever outbreak that has fuelled inflation and hit consumer spending.

Image copyright GETTY IMAGESImage caption China accounted for 16% of global gross domestic product in 2018, according to the McKinsey Global Institute

This week the International Monetary Fund trimmed its 2019 growth forecast for China to 6.1% from 6.2% due to the long-running trade dispute and slowing domestic demand.

But there have been some signs of progress toward resolving the trade battle, with the US and China reaching a “phase one deal” earlier this month.

Any analysis of China’s economic data has to come with a caveat: Many economists believe the actual figures are much lower than what we are told, but it’s the trajectory of growth and signalling from the government that you should pay attention to.

The fact that the growth figures have come in below market expectations indicate that China’s economy is hurting more than many thought.

There were signs from China that these numbers were going to be worrying. Earlier this week, Premier Li Keqiang made the unusual move to warn local officials that they must do “everything” to make sure they hit growth targets for this year.

China’s economy is being hit on three fronts: The US-led trade war, slowing demand at home and rising domestic challenges including the outbreak of swine fever that has dealt a huge blow to its pork farmers. It’s also pushed up prices for consumers.

China’s slowdown is nothing new. But these challenges pose new headaches for policymakers who are trying to manage the slowdown. The country’s political stability depends on economic security – and over the last forty years, that’s what the Communist Party has delivered. They’re under pressure to keep that contract.

‘Forbes’ magazine reported that China’s central bank will launch its own sovereign digital currency to coincide with the Singles’ Day online shopping festival

The People’s Bank of China is seeking to address financial risks and counter the current dominance of the US dollar

The Singles’ Day is a holiday celebrated in China on November 11 and has become the largest online shopping day in the world. Photo: Simon Song

China’s desire to launch the world’s first government-backed digital currency could see the possible rival to Facebook’s Libra be launched in time for November’s Singles’ Day online shopping festival despite a Chinese media report playing down the timing as “inaccurate speculation”.

Several central bank officials have publicly spoken out over the past several weeks about the need for China to launch its own digital currency since Facebook unveiled its plans for Libra, and the People’s Bank of China (PBOC) appear to be making rapid progress ahead of an expected launch.

Forbes magazine reported this week, citing a source who previously worked for the Chinese government, that China’s central bank could launch the digital currency as soon as November 11 as its bids to address financial risks and to counter the current dominance of the US dollar.

The PBOC did not respond to a faxed request for comment on the Forbes story, although Sina.com said that the report was “inaccurate speculation” citing an unnamed source close to the central bank.

China’s central bank is expected to distribute its digital currency through the big four state-owned banks – the Industrial and Commercial Bank of China, China Construction Bank, the Agricultural Bank of China, and the Bank of China – and mobile payments systems Alipay and WeChat Pay, as well as UnionPay, the state-supported credit card provider, according to the Forbes report. Alibaba is the owner of the South China Morning Post.

Ma Changchun, deputy chief of the Payment and Settlement Division of the PBOC, said at the start of August that a digital currency prototype existed and that the central banks’ Digital Money Research Group had already fully adopted blockchain architecture to ensure its use in retail transactions.

“The People’s Bank digital currency can now be said to be ready,” said Ma on August 11.

The People’s Bank digital currency can now be said to be ready Ma Changchun

Former central bank governor Zhou Xiaochuan said last month that, in addition to central banks, “commercial entities” should be allowed to issue banknotes backed by their own private currency assets, although he did not elaborate on what kind of “commercial entities” might be appropriate to issue a digital currency in China.

China is also ready to make Shenzhen a pilot zone for digital currency as part of plans for the city to become a socialist model city, according to a statement summarising a meeting between the Shenzhen party secretary Wang Weizhong and central bank governor Yi Gang released on Thursday.

The PBOC implemented a blanket crackdown in China on trading of cryptocurrency, including bitcoin, which are not backed by any government, viewing them as risks to China’s financial stability and security. At the same time, in 2014 the central bank created its own academy to study digital currencies and the related blockchain technology.

Neil Woodfine, director of marketing at blockchain start-up Blockstream, said a digital currency created by the PBOC would be “just like cash” and “would be fully controlled by the central bank.”

“If it’s digital instead of physical, they can close accounts and monitor all activities [in the entire financial system]. Commercial bank deposits are difficult for them to monitor, control or pull information out of for verification because the numbers are in each bank’s data centre,” Woodfine said.

Wang Xin, director of the central bank’s research bureau, said last month that

to create its own digital currency have pushed Beijing to speed up its own digital currency plan as Libra could potentially pose a challenge to Chinese cross-border payments, monetary policy and even financial sovereignty.

Leonhard Weese, the president of the Bitcoin Association of Hong Kong, said that a government-backed digital currency may enhance the PBOC’s control of China’s monetary system, cutting reliance on commercial banks to transmit changes in monetary policy.

“It would be similar to just killing the commercial banks,” Weese said.

which would be a non-sovereign digital currency controlled by a Swiss-based company, has come under intense scrutiny by regulators and central banks worldwide. Last month, the Group of Seven industrialised nations, known as the G7, called for urgent regulatory measures and other types of action to address serious concerns over Libra.

Central banks, however, have expressed interest in launching their own digital currencies to counter the US dollar and to gain more control of their own monetary systems.

Mark Carney, governor of the Bank of England, argued last week that the US dollar, the current dominant reserve currency, could be replaced by a global digital alternative to tackle ultra-low interest rates.

Facebook’s Libra, which is expected to be launched next year, will be pegged to a basket of convertible currencies – so it could serve as a stable online currency – while its payments will be endorsed by Visa and Mastercard. Photo: Reuters

A digital currency “could dampen the domineering influence of the US dollar on global trade”, Carney said last week at the US Federal Reserve’s annual conference, adding that a digital currency has the edge to counter shocks emanating from the US through trade and exchange rates.

Daniel Wang, chief executive and co-founder of blockchain start-up Loopring, said that a Chinese government-backed digital currency may provide a new way for the yuan to compete globally.

“If the central bank wants to increase the global competitiveness of the yuan through its digital currency, only an open and standard-based competitor carries any hope,” said Wang.

A digital yuan would “remain a sovereign currency under a centralised sovereign,” continuing to require the trust from users in the Chinese central bank and government institutions behind it, Wang added.

Alfred Schipke, senior resident representative for China at the International Monetary Fund (IMF), said that the bank is “open” to digital currencies, including the one being developed by China’s central bank.

The IMF in principle is looking at these things favourably. It’s a two-way process where we learn from China, which is often at the forefront of development. Alfred Schipke

“We don’t have a specific view on a particular currency, we haven’t looked at the details of the latest proposals from China,” Schipke said on Thursday. “The IMF in principle is looking at these things favourably. It’s a two-way process where we learn from China, which is often at the forefront of development.”

Blockstream’s Woodfine said that Beijing’s move also reflects a growing concerns among central banks that a financial disaster is on the horizon.

The 30-year US Treasury bond yield fell to an all-time low 1.976 per cent on Thursday, while yields around the world also plunged to multi-year or record low, triggering rising fears over a global recession.

Central banks around have also been driving down interest rates, with the PBOC recently unveiling a key interest rate reform that effectively cuts borrowing costs for companies to boost its slowing economy.

“We’ll see a move by governments and central banks to take back control over the financial system and use that power to direct their economies, continuing to pump money into the system to keep it afloat,” Woodfine added.

“A digital currency would be the perfect channel for helicopter money,” he said in reference to the idea that a central bank could stimulate the economy by giving out large quantities of money to the public, as if dumped from the sky. “They can send out free money to consumers.”

Beijing has lent billions of dollars to countries on the continent to build railways, highways and airports but critics say the borrowings are unsustainable

Chinese officials say the projects will pay off in the long run and host nations are well aware of their limits and needs

Illustration: Lau Kakuen

When Clement Mouamba went to Beijing last year, he had two main tasks.

The prime minister of the Republic of Congo needed to find out exactly how much his country owed to China, a number the struggling, oil-rich central African nation had until then not been able to provide the International Monetary Fund (IMF) to qualify for a bailout. He also needed to convince Beijing to restructure its debt to ensure sustainability.

The IMF had put talks for further loans on hold until Mouamba’s administration could say exactly how much it had to repay to the country’s external creditors, including China – the republic’s single largest bilateral lender – and oil multinationals such as Glencore and Trafigura.

The country, which heavily depends on oil revenue, turned to China and private oil majors for funding to run the government when in 2014 oil prices fell from a high of US$100 per barrel to as low as US$30.

The Republic of Congo has since restructured its borrowings from China, which holds about a third, or US$2.5 billion, of the Congolese debt, by extending the repayment period by an additional 15 years.

A number of other African countries struggling to service their loans from Beijing have also pursued concessions. Ethiopia has had part of its Chinese debt written off and terms relaxed for the US$3.3 billion loan it took to build its railway, while Zambia is seeking similar adjustments for its borrowings used to build airports and highways.

Critics say countries on the continent are being burdened with unrealistic levels of debt for inviable infrastructure backed and built by China without adequate transparency and scrutiny.

The biggest concern is that several African countries will be left with huge debts and grandiose infrastructure that they cannot maintain and run profitably. I liken it to borrowing money to buy a Tesla when you don’t have adequate access to electricity: Obert Hodzi of the University of Helsinki in Finland

But Chinese observers say the West must take some of the blame for the countries’ debt problems and that the support China offers will benefit the host countries in the long run.

In the early 1990s, when China began to embrace Africa again after years of isolation from the outside world, the aspiring manufacturer was at a serious disadvantage in the race for raw materials and markets for its industrial goods.

The former colonial powers of the West had already sewn up deals for many of the continent’s most lucrative and readily exploitable reserves, from fossil fuels to minerals.

China needed new strategies to convince African governments to allow it access raw materials for its industries and markets for its products to a largely unfamiliar partner.

China also wanted to challenge the dominance of the US in global trade and politics so it courted allies in Africa to help it push for political legitimacy in international institutions.

A Kenya Railways freight train leaves the port station on the Mombasa-Nairobi railway in Mombasa, Kenya, a huge project backed by China. Photo: Bloomberg

At the time, many African leaders were under fire to liberalise their economies. China’s approach was to promise not to meddle in individual country’s internal affairs and assure African countries that they could get billions in exchange for future delivery of minerals through resource-backed deals.

Beijing sold its policies that it had no conditions attached to its development finance. In the drive to drum up business, China promised affordable loans for African countries to build roads, bridges, highways, airports and power dams.

Is Kenya’s Chinese-built railway a massive white elephant?

But Beijing also pursued tied finance, ensuring that countries borrowing from China used Chinese contractors to implement the projects rather than open them up to outside bids.

In addition, many of the deals were built on weak financial, technical and environmental conditions, with Chinese state firms conducting the technical feasibility, environmental impact assessment and financial viability studies for free for projects that they also build.

For example, in Kenya, the China Road and Bridge Corporation conducted a free feasibility study that was used in the construction of the railway.

The same company was handed the contract to implement the project and is operating both the passenger and cargo train service for a fee.

Chinese companies were responsible for the construction of a rail line between Addis Ababa and Djibouti. Photo: AFP

In contrast, the World Bank and its partner institution, the IMF, demand that such studies be done by an independent consultant and not by the company that implements the project.

According to data compiled by the China-Africa Research Initiative, at the Johns Hopkins University School of Advanced International Studies, Beijing has advanced loans worth US$143 billion to African countries since 2000, levels that some critics say are unsustainable for the borrowers.

China meets resistance over Kenya coal plant, in test of its African ambitions

For many of China’s new African partners, these arrangements – from easy lending terms, to non-competitive bidding and opaque contract details – have led to new problems – problems that corrupt or poorly managed governments now share substantial responsibility.

Some critics, both in the West and in host countries, suggest there is a “debt-trap strategy” at the heart of Beijing’s push for international business and influence, but there is no evidence that China deliberately pushes other countries into debt to seize their assets or gain sway.

However, the drive for overseas contracts and big business has led some countries into difficulties with new debts, and there are question marks over the viability of many of the projects the money is funding.

Obert Hodzi, an international relations expert at the University of Helsinki in Finland, said the Addis Ababa-Djibouti railway and the Mombasa-Nairobi railway were good examples of huge projects that were financed by easy borrowing terms from China but were not sustainable and that had in turn forced the African partners to seek further Chinese help.

“The biggest concern is that several African countries will be left with huge debts and grandiose infrastructure that they cannot maintain and run profitably,” Hodzi said. “I liken it to borrowing money to buy a Tesla when you don’t have adequate access to electricity.”

Ken Opalo, a Kenyan scholar at Georgetown University in Washington, said the key issue was the inability of African countries to design projects that were actually needed for the local economies.

A road is not just a means of transport but an economic belt or corridor that will catalyse the development of the whole region: Huang Xueqing, spokeswoman for the Chinese embassy in Nairobi

“Most African countries have been willing to accept projects designed, financed, and implemented by Chinese firms,” Opalo said.

“It would be better to decouple the feasibility studies and design phases of projects from the financing. That way African governments can ensure that they are truly getting value for money.”

But Chinese officials said Beijing had invested in infrastructure largely at the request of the host countries, adding that it could take time to yield returns on the projects.

Huang Xueqing, spokeswoman for the Chinese embassy in Nairobi, said the projects were valid assets with value that would grow in time.

“So, in the long run, it is beneficial to the host countries. Just like when young people buy a house with a mortgage, they may take some debts, but they have a place to live in and have their own assets,” Huang said.

“Underdeveloped infrastructure is the bottleneck that has been holding back Africa’s development. Up to today, many African countries, although in the same continent, are not connected with direct flights, railways or even roads. You have to fly to Paris or Zurich in order to get to some African countries.

“A road is not just a means of transport but an economic belt or corridor that will catalyse the development of the whole region.”

Huang said Beijing had advised the countries to act within their means and not to overstretch themselves when they considered projects that might not be in line with local conditions.

“When making investment decisions, the Chinese side, along with the recipient countries, carry out rigorous feasibility studies and evaluations. We do things according to our ability,” she said.

China’s leadership has also said it is paying close attention to the fiscal and financial difficulties faced by some African countries.

“As a good friend and good brother … the Chinese side is willing to lend a helping hand when needed by the African people to help them overcome temporary difficulties,” State Councillor and Foreign Minister Wang Yi said in January while on a trip to Ethiopia, adding that the debt situation in Africa is also a legacy issue.

China must allay any debt-trap fears in its dealings with Africa

“The African debt issue does not come up today, still less is it caused by the Chinese side. The African people know who are the initiators of African debt.”

The West should take a lot of the blame for worsening debt problems in some African countries, according to Li Anshan, from Peking University’s Centre for African Studies.

He cited the cases of Liberia and the Democratic Republic of Congo, two countries that have had close relations with the West for many years but remain ravaged by war and poverty despite immense natural resources.

“China-Africa relations have been going on for quite some time. Is there any African country which has got poorer because of its deal with China?” Li said.

Gyude Moore, a former Liberian minister of public works whose department oversaw construction and maintenance of various public infrastructure funded and built by China, said it would be difficult to imagine that China would knowingly ensnare its partners in debt.

“China attempts to differentiate itself from Western donors by limiting non loan-related conditionality. China also practices non-interference, so how a country manages its resources, treats its people or deploy its finances were considered ‘internal’,” he said.

“So, Chinese loans are negotiated faster and place less emphasis on public financial management.”

Moore, now a visiting fellow at the Centre for Global Development, said there were trade-offs in such situations.

China focuses on sustainable projects to dismiss fears of African debt trap

“If the loans are going to be fast – the due diligence will not be as rigorous. Chinese project selection mixes political with economic considerations. So, while a project may not make as much economic sense, it may pay political dividends,” he said.

He said non-transparent processes would invite abuse, be they Chinese, Western or African.

Other observers say the question of opacity is more directly related to China’s own economic system.

Howard French, author of China’s Second Continent: How a Million Migrants are Building a New Empire in Africa, said China has very limited transparency and public accountability in its own domestic processes.

The Mombasa railway station is seen in Mombasa, Kenya, in 2018. Photo: Xinhua

“So it would be unusual to expect that China would introduce greater transparency and accountability in its dealings with African countries than it is used to at home – that is, unless African governments insist on it,” French said.

“And this is where African governance comes in. African states should insist on contract transparency but often don’t do so because that offers leaders plentiful opportunities for graft.”

David Shinn, professor of international relations at George Washington University in Washington, agreed that China’s lack of loan transparency was a huge problem and increased the risk of corruption on both the African and Chinese sides. But he also said that in some cases, African governments might have negotiated poorly.

“This is, however, the responsibility of the African government. I don’t think China is purposely trying to encourage African debts in order to gain leverage,” Shinn said.

“In fact, China is becoming more careful about its lending because it is concerned it has made too much credit available to some African countries.”

China ‘ready to talk’ about trade deal with East Africa bloc

Huang Hongxiang, director of China House, a Nairobi-based consultancy that helps Chinese in Africa integrate better, agreed, saying the Chinese government needs to communicate more about projects in Africa but African countries also have a bigger part to play in ensuring better deals.

“On commercial viability, accountability, transparency and governance, I believe the responsibility does not lie with China, the US or the West but in the hands of African countries,” he said.

Wherever the fault lies, one thing is clear when money is wasted on ill-designed projects that have little to no economic return, according to Opalo.

“The lack of planning and transparency creates default risks … [and] African taxpayers will be left holding the bag.”

This article is the third in a series examining the local impact of Chinese investment and infrastructure projects in Africa. Read part one here and part two

Image copyright GETTY IMAGES

Image copyright GETTY IMAGES Image copyright GETTY IMAGES

Image copyright GETTY IMAGES